Client Advisory Letter ( March 2018)

This is a publication about developments in Philippine taxation. The contents usually include latest Republic Acts, Bureau of Internal Revenue issuances, Customs regulations, Court decisions, BSP circulars, SEC circulars, Department of Justice opinions and Executive Orders relevant to Tax practice.

Talk to us

For further discussion on the contents of this issue of the Client Advisory Letter, please contact any of our partners.

Request for copies of text

You may ask for the full text of the Client Advisory Letter by writing our Tax Department, Isla Lipana & Co., 29th Floor, Philamlife Tower, 8767 Paseo de Roxas, 1226 Makati City, Philippines. T: +63 (2) 845 2728. F: +63 (2) 845 2806.

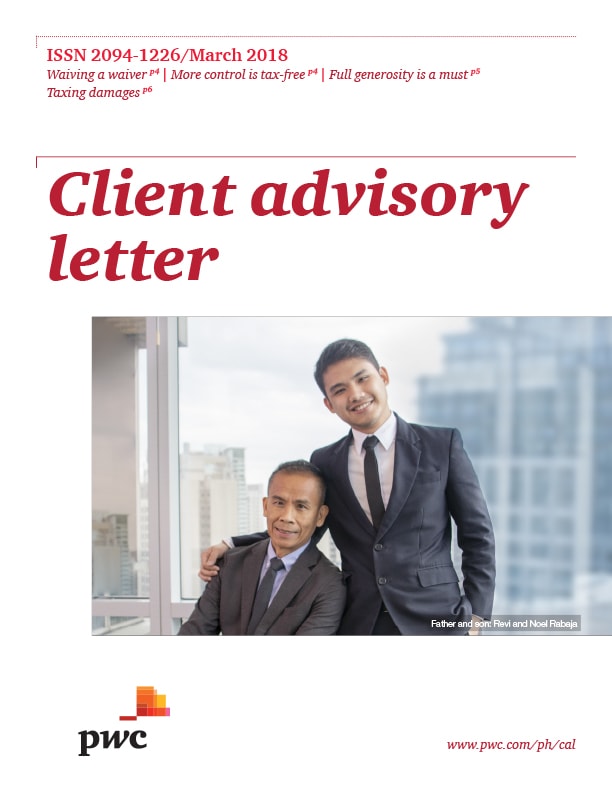

About our cover photo: Noel’s father, Revi, is one of the firm’s current employees who started with Joaquin Cunanan & Co. (JCC) during Price Waterhouse days. Noel’s mother, Dorie, spent three years with JCC. Then Revi worked elsewhere until he decided to return to PwC in February 2007. He is now a Client Accounting Services (CAS) Senior Manager while Noel is a Risk Assurance Associate.

Although both of his parents are CPAs, Noel did not see himself as becoming one. But good friends and self-motivation may have encouraged him to pursue accountancy. And the rest is history.

Committee decides how to present interest revenue

At a glance

The IFRS Interpretations Committee has concluded that the line item ‘interest revenue’ can contain only interest income on assets that are measured at amortized cost or fair value through other comprehensive income (subject to the effect of applying hedge accounting to derivatives in designated hedge relationships).

This will be a change to current practice for some entities. It is likely to have the most significant impact on financial services entities, such as banks for whom interest revenue or net interest margin is a key performance indicator.

What is the issue?

IFRS/PFRS 9 introduced a consequential amendment to paragraph 82(a) of IAS/PAS 1, under which interest revenue calculated using the effective interest method is required to be presented separately on the face of the income statement.

The IFRS Interpretations Committee (the ‘Committee’) has issued an agenda decision which concludes that this separate line item can be used only for interest on those financial assets that are measured at amortized cost or fair value through other comprehensive income (subject to the effect of applying hedge accounting to derivatives in designated hedge relationships).

This means that interest income on items that are not measured at amortized cost or fair value through other comprehensive income will no longer be able to be included in interest revenue.

What is the impact?

This change is likely to have the most significant impact on financial services entities, such as banks. Some such entities currently include interest income on certain assets measured at fair value through profit or loss (‘FVTPL’) in interest revenue, but they will no longer be able to do this.

Depending on an entity’s existing presentation policy, this change might impact the presentation of gains and losses on some or all of the following:

derivatives including ‘economic hedges’ to which hedge accounting has not been applied; however, where hedge accounting is applied, hedging gains and losses can continue to be presented in interest revenue

non-derivative assets to which the fair value option has been applied

non-derivative assets that fail the ‘solely payments of principal and interest’ requirements in IFRS/PFRS 9

non-derivative assets that fall within the ‘other’ business model in IFRS/PFRS 9.

Can additional line items be presented?

Some entities might wish, as a matter of accounting policy, to present additional line items, on the face of the income statement, for ‘interest’ on instruments measured at FVTPL. While not addressed by the Committee, IAS 1 permits an entity to present additional line items where doing so is relevant to an understanding of the entity’s financial performance. If such a presentation is adopted, the additional line items should be appropriately presented and labelled. Also, the entity’s accounting policy, including how such amounts are calculated and on which instruments, should be disclosed.

What is the impact?

The Committee’s agenda decision is effective at the same time as IFRS/PFRS 9 (that is, for accounting periods beginning on or after 1 January 2018).

Taxes, compliance matters, assessments and refunds

Waiving a waiver

BIR wasted the validated defective waiver

The SC again ruled that a defective waiver is valid if the taxpayer benefited from it and failed to question the same at the earliest possible time.

In this case, it was only before the CTA that the taxpayer questioned the validity of the waivers on the basis that the taxpayer’s representative who signed the waivers has no authority. The SC also found that the taxpayer, in its protest letter to the FAN, clearly admitted the validity of the waivers it executed. Although the waivers are defective, the SC declared that the taxpayer is estopped from questioning the validity of the waivers.

Nevertheless, the SC found that the assessment was served beyond the period extended by the validated defective waivers. Thus, the High Court eventually voided the assessment.

(GR No. 227544 dated 22 November 2017)

More control is tax-free

The CTA En Banc affirmed the tax-free treatment of share swap for further control

In a share swap agreement, the taxpayers’ shareholding in the retail company increased from 66.55% to 75.83%. Prior to the share swap, the taxpayers already collectively owned more than majority of the outstanding capital stock of the retail company. The taxpayers treated the share swap as tax-free exchange under Sections 40(C)(2) and (6)(c) of the Tax Code. The tax office opposed the treatment on the basis that the taxpayers failed to secure the required application for a tax-free exchange certification from the BIR.

The CTA En Banc upheld the decision of the CTA Division which ruled that the share swap transaction qualifies for tax-free exchange treatment under Sections 40(C)(2) and (6)(c) of the Tax Code. The CTA reiterated that a BIR ruling is not a prerequisite for the tax-free exchange treatment. Under the law, no gain or loss shall be recognized if the property is transferred to a corporation by a person in exchange for stock in such a corporation of which, as a result of such exchange said person, alone or together with others, not exceeding four persons, gains control of said corporation. In this case, the control requirement is sufficiently met when after the transfer, the taxpayers further increased their equity to more than 51% of the total voting power in the transferee corporation. Consequently, the transferor will not be subject to CGT, income tax or creditable withholding tax on the transfer of such property.

(CTA EB No. 1522 dated 28 February 2018)

Must pay for exemption

Pay under protest if RPT assessment is questioned based on tax exemption

A taxpayer corporation questioned the Notices of Assessment (NOA) and the Tax Declarations it received from the Municipal Assessor, arguing that it is exempt from payment of RPT. The corporation’s petition was dismissed on the ground that it failed to pay first the tax under protest before filing an appeal.

Citing an SC decision1, the CTA En Banc explained that a taxpayer may protest an RPT assessment in either of the following ways: first, file a protest which questions or challenges the reasonableness or correctness of the assessment; or second, file a protest which questions the legality or validity of the assessment. If a taxpayer’s protest falls on the first kind, then Section 252 of the Local Government Code mandates that such protest to the city or municipal treasurer must be preceded by payment of the assessed RPT. Should the protest fall on the second type, then the taxpayer must file the protest to the proper court.

The CTA ruled that a claim of tax exemption is not considered as a protest, which questions the authority of the local assessor to assess, but merely raises a question of reasonableness or correctness of the assessment. Thus, it requires the payment of the assessment under protest. It must be noted that the exemption of certain real property from RPT is not automatic, but involves a process by which the provincial, city or municipal assessor evaluates various documents submitted by the taxpayer to prove entitlement to such exemption.

(CTA EB No. 1459 dated 27 February 2018)

1 GR No. 171596 dated 25 January 2010

Full generosity is a must

Paying allowances to board of trustees amounts to distribution of profit

A bible-evangelical Church applied for a tax exemption certificate as a non-stock, non-profit association under Section 30(e) of the Tax Code. The BIR denied the application based on findings that the board of trustees of the association receive honorarium and allowances. This is considered a distribution of equity (including net income), which is in violation of the requirement for tax exemption. For the exemption to apply, no part of the income or assets of the corporation must inure to the benefit of any trustee, officer, member or any specific person.

(BIR Ruling No. 060-2018 dated 24 January 2018)

Excise on the loose

Empty cigarette tubes are exempt, while loose tobaccos are subject to excise tax

In a request for a legal opinion, the following issues were raised: first, whether the sale of cigarette tubes and loose tobaccos directly to end users is subject to excise tax; and second, whether the excise tax shall be based on kilogram or per pack.

The BIR ruled that only tobacco products enumerated in Section 144 of the Tax Code are subject to excise tax. An empty cigarette tube, without any tobacco or substitute smoking material in it, is not covered by Section 144, nor does it qualify as cigarette subject to excise tax under Section 145 of the Tax Code.

However, loose tobacco, as a general rule, is subject to excise tax under Section 144 of the Tax Code except if it is exported or used in the manufacture of cigars, cigarettes, or other tobacco products on which the excise tax will eventually be paid on the finished products. Since, in this case, the sale of loose tobacco is made to end users, it is subject to excise tax at the rate of PHP1.75 per kilogram pursuant to Section 144 of the Tax Code.

While the cigarette tube is not subject to excise tax, it may be considered as a regulated raw material if made of cigarette paper pursuant to Section 260 of the Tax Code. In which case, the taxpayer is required to register with the ELTRD and to secure from the said office a Permit to Operate for excise tax purposes, pursuant to Section 154 of the Tax Code, as amended, and RMO No. 38-2003.

(BIR Ruling No. 032-2018 dated 23 January 2018)

Inventing for exemption

Tax exemption on local inventions refers to income tax only

In a request for tax exemption under Section 6 of RA No. 7459, otherwise known as the “Inventors and Inventions Incentives Act of the Philippines,” the BIR clarified that while an inventor is exempt from tax during the first 10 years from the date of the first sale, the exemption is not absolute. Based on the Final Resolution of the Office of the President (OP) in OP Case No. 03-G-422 dated 2 February 2004, the exemption merely refers to income tax. This exemption is extended to the inventor, and on his legal heir or assignee upon the death of the inventor. It does not apply, however, to any other entity that commercially produces and distributes the invented product. Thus, the taxpayer is granted income tax exemption only on income arising from his invention.

BIR Ruling No. 537-2017 dated 20 November 2017)

Taxing damages

Taxability of awarded damages in a civil case

On the issue of whether damages awarded in a civil case for murder is part of the taxable income of the heirs of the decedent, the BIR clarified that, as a general rule, compensatory damages, actual damages, moral damages, exemplary damages, attorney’s fees, and the cost of the suit, are excluded from gross income of the awarded party pursuant to Section 32(B)(4) of the Tax Code and Section 63 of RR No. 02-40. However, consequential damages representing the loss of the victim’s earning capacity are not excluded from gross income. Such damages are merely replacement of income which would have been subject to tax if earned.

As to whether the transfer of real property, arising from a court decision in a civil case for annulment of sale in fraud of creditors with damages, is subject to CGT and DST, the BIR qualified as follows:

- The current fair market value (FMV) of the property, which corresponds to the award of compensatory, actual, moral, and exemplary damages, attorney’s fees, and the cost of the suit, is exempt from CGT and DST.

- On the other hand, the current FMV of the property which corresponds to the amount of consequential damages representing loss of the victim’s earning capacity, including legal interest of 6%, is subject to CGT and DST. The legal interest shall be reckoned from the last day of filing of CGT and DST in accordance with Section 2 of RR No. 9-2012.

(BIR Ruling No. 26-2018 dated 18 January 2018)

Access granted

Authority of Commissioner to obtain third party information

The power of the Commissioner to obtain information under Section 5 of the Tax Code serves as an exception to both the attorney-client and accountant-client privilege. Thus, in ascertaining the correctness of any return, in making a return when none has been made, in determining the liability of any person for any internal revenue tax, in collecting any such liability, or in evaluating tax compliance, the Commissioner may obtain from any person, other than the person whose internal revenue tax liability is subject to audit or investigation, any information as may be needed.

(Revenue Memorandum Circular No. 12-2018 dated 22 February 2018)

TRAIN continues

Guidelines for AABs in processing BIR Form No. 0605

All Authorized Agent Banks (AAB) are hereby advised to accept all payments for whatever purpose using the BIR Form No. 0605 even without the required approval or signature by the authorized BIR personnel in relation to the implementation of RA No. 10963, otherwise known as the “TRAIN Law.” Also, taxes withheld within the first two months of every taxable quarter shall be remitted through BIR Form No. 0605 on or before the 10th day (for over-the-counter filers) or 15th day (for eFPS filers) of the following month of withholding until an enhanced monthly withholding remittance form is available. The Alphanumeric Tax Code (ATC) to be used in filing/remittance of withholding tax shall be “MC 200” and the Tax Type shall be “WE” for expanded withholding tax or “WF” for final withholding tax.

(BIR Bank Bulletin No. 2018-02 dated 7 February 2018)

New regulations on the amended income tax provision

This issuance contains the implementing rules for the TRAIN Law, promulgated to implement the amended provisions on Title II - Tax on Income of the Tax Code. It provides for the new income tax rates for individual citizens/individual resident alien (Section 3), non-resident alien individuals (Section 4), GOCCs/agencies (Section 5), exclusions from gross income (Section 6), special treatment of fringe benefits (Section 7), deductions from gross income (Section 8), individuals not required to file ITR (Section 9), time of filing of ITR (Section 10), installment payment (Section 11), and registration updates (Section 12).

(Revenue Regulations No. 8-2018 dated 25 January 2018)

Guidelines on the amended percentage tax and VAT provision

The filing of percentage tax returns shall be made on a quarterly basis as reiterated in the TRAIN Law. However, taxpayers who are required to withhold OPT and VAT under RR No. 2-98 shall continue to withhold and remit taxes on a monthly basis using BIR Form No. 1600.

In view of the increase of the exemption from VAT on gross annual sales/receipts not exceeding PHP3m, existing VAT-registered persons who need to update the registration of their tax type on business from VAT to OPT must do so by accomplishing BIR Form No. 1905, except those who opt to remain as VAT-registered.

Self-employed individuals who opt to avail of the 8% income tax on gross sales or receipts need to accomplish BIR Form No. 1905 to effect the end date for their VAT or OPT registration, and as such, they are not required to file quarterly percentage tax returns. All concerned taxpayers are advised to strictly comply with the guidelines for transactions starting 1 January 2018.

(Supplemental Tax Advisory dated 19 February 2018)

Processing of claims for TCC in relation to the TRAIN Law

This issuance amends RMC No. 89-2017 and certain provisions of RMC No. 54-2014 regarding the processing of claims for issuance of tax refund/TCC in relation to amendments introduced by the TRAIN law.

(Revenue Memorandum Circular No. 17-2018 dated 27 February 2018)

Regulation implementing the increase in stock transfer tax

Pursuant to the TRAIN Law, tax on the sale, barter or exchange of shares of stock listed and traded through the local stock exchange shall be levied, assessed and collected at the rate of six-tenths of one percent (6/10 of 1%) of the gross selling price or gross value in money of the shares of stock. The percentage tax on the sale, barter or exchange of shares of stock listed and traded through the local stock exchange has been increased from one-half of one percent (1⁄2 of 1%) to six-tenths of one percent (6/10 of 1%).

(Revenue Regulations No. 9-2018 dated 26 February 2018)

Throwback

ICC applications no longer accepted by BIR

Effective 1 March 2018, BIR will no longer accept applications for the ICC and BCC pursuant to DOF DO No. 011-2018 dated 9 February 2018, which reverted the authority to accredit and to register customs brokers and importers solely to the BOC.

(BIR Advisory dated 26 February 2018)

Let me know

Amendment to the exchange of information regulation

Under the new rule, amending Section 10 of

RR No. 10-2010, or the “Exchange of Information Regulations,” a taxpayer shall be duly notified by the CIR, when a foreign tax authority is requesting for exchange of information held by financial institutions pursuant to an international convention or agreement on tax matters, within 60 days following the transmittal of all the information requested from, and provided for by the concerned financial institution to the requesting treaty partner.

(Revenue Regulations No. 10-2018 dated 26 February 2018)

Status quo on PEZA

TRAIN law does not affect zero-rating on sale to PEZA locators

The PEZA maintains status quo on VAT zero-rating incentives on sales of goods or services to separate customs territory. This is pursuant to Section 8 of RA No. 7916, otherwise known as the “Special Economic Zone Act of 1995,” which provides that special economic zones are to be operated and managed as separate customs territory. The provision has not been amended or repealed by the TRAIN Law. Thus, absent any contrary or incompatible law or revenue regulation, the VAT zero-rating incentive being enjoyed by PEZA locators shall remain in full force and effect.

(PEZA Memorandum Circular No. 2018-003 dated 12 March 2018)

Latest on regulatory landscape

MLR report compliance

Guidelines on the electronic submission of the MLR report

The BSP issued guidelines for the electronic submission of the MLR report during the observation period from 1 January to 31 December 2018. All covered BSP Supervised Financial Institutions are required to submit the MLR report quarterly on a solo basis to BSP-Supervisory Data Center (SDC). The prescribed Data Entry Template and Control Proof List of the MLR Report can be downloaded from http://www.bsp.gov.ph/SES/reporting_templates or requested from the BSP-SDC.

(BSP Memorandum No. M-2018-007 dated 22 February 2018)

M&As getting bigger

Adjustment of the threshold for notification in mergers or acquisitions

Reflecting inflation and economic growth, the Commission amended Rule 4, Section 3 of the IRR of RA No. 10667, otherwise known as the “Philippine Competition Act,” by increasing the initial thresholds for compulsory notification in mergers and acquisitions. Parties are now required to provide notification when: (a) the aggregate annual gross revenues of all entities exceed five billion pesos, and (b) the value of the transaction exceeds two billion pesos.

(PCC Memorandum Circular No. 18-001 dated 1 March 2018)

Standard chart for brokers

Rules on financial reporting framework

To ensure transparent and consistent application of the rules on financial reporting framework, recognition and measurement of accounts are required from brokers to be in accordance with the current generally accepted accounting principles in the Philippines at the reporting date. This circular provides a standard chart of accounts for brokers which consists of economic valuation of assets and liabilities.

(Insurance Commission Circular Letter No. 2018-17 dated 9 March 2018)

Follow PwC Philippines