The key question for business leaders on CSRD isn’t about mere compliance. Rather it should be — How will your company create value in a world focused on sustainability?

This question can be answered in a host of ways — with answers touching on net-zero targets, decarbonisation pathways, efforts to design green products and services, circular-economy projects and myriad other aspects of sustainability. The best way for business leaders to view CSRD is through the lens of the opportunities that sustainability presents — not as a box-ticking exercise.

Corporate Sustainability Reporting Directive more than just reporting, it drives business transformation and has an impact on multiple business processes. The Directive encourages a more thorough, structured approach to strategic planning and sustainable transformations. The adoption of the Directive highlights the importance of implementing sustainable business practices and enhancing the transparency and reliability of non-financial reports. CSRD is the new reality for businesses in the EU and Ukraine alike. Our expert team helps businesses adapt to the new regulatory requirements, provides specialised advice and shares experience in the area of CSRD.

Leaders should look beyond the compliance elements of CSRD and align business and strategy on sustainability factors which can also drive stronger financial results.

This approach calls for executive teams to make four shifts in the way they manage their business: to integrate sustainability in strategy, recognise companies’ impact on the world, improve decision-making and produce more useful data. Read more in this Global PwC article on CSRD.

CSRD at a glance

- What is CSRD?

- Which firms are affected?

- What’s required?

- Who’s responsible?

- What is the CSRD implementation timeline?

What is CSRD?

The EU’s Corporate Sustainability Reporting Directive (CSRD) is an incoming piece of regulation. It requires companies to make extensive, detailed disclosures about sustainability performance and related strategic implications. Disclosures are prescribed by European Sustainability Reporting Standards (ESRS)

The ESRS are reporting standards for sustainability within the EU that cover a multitude of environmental, social, and governance (ESG) topics — including climate change, biodiversity, human rights, etc. The primary purpose of ESRS is to enable a simple and logical structure of sustainability information. The standards are an integral part of the CSRD and there are a comprehensive set of 12 ESRS in operation, with more in the pipeline.

Which firms are affected?

All companies listed on EU-regulated markets and large companies not listed — potentially including non EU-based multinational companies. CSRD is expected to impact approximately 50,000 companies globally — including 10,000 companies headquartered outside of the EU and include those in the following categories:

Companies with securities listed on an EU-regulated market (with some exceptions, such as ‘micro-undertakings’).

Unlisted EU companies of a certain size (including EU subsidiaries of companies headquartered outside the EU, which may be covered by the parent companies’ consolidated reporting).

Unlisted EU parent companies with total holdings of a certain size. [1]

[1] Companies must comply with CSRD if they exceed two of the following three size thresholds: total assets of €25 million, revenue of €50 million and an average of 250 employees during the fiscal year on two consecutive balance-sheet dates..

What’s required?

Companies must assess the materiality of sustainability topics across their value chains and consider which of more than 1,000 data points to disclose. Other disclosures will consist of qualitative information, such as how the corporate strategy accounts for sustainability opportunities and risks. All the information requires independent assurance (beginning at the limited level).

Who’s responsible?

Chief Executive Officers, Chief Financial Officers, Chief Security Officers and Chief Information Officers — indeed entire management teams — will have new day-to-day CSRD tasks. Supervisory boards and audit committees must oversee a company’s sustainability reporting.

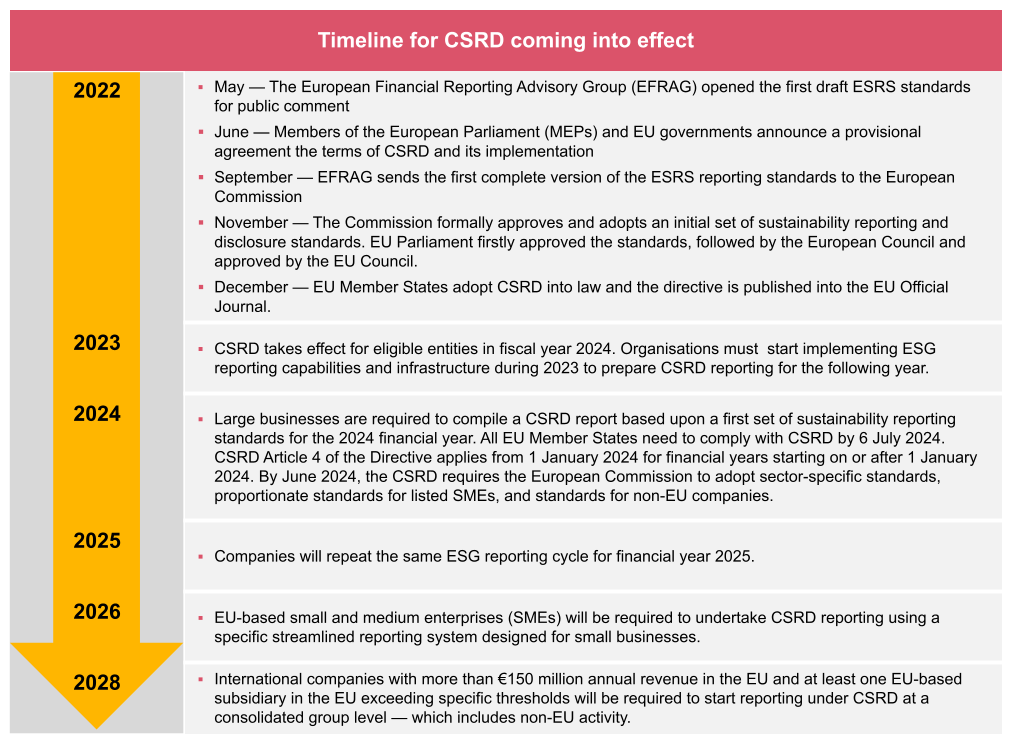

What is the CSRD implementation timeline?

Companies now subject to the EU’s Non-Financial Reporting Directive must follow the Directive for fiscal years starting on or after January 1 2024 (filing reports in FY2025). Other listed companies, along with unlisted companies meeting certain size thresholds, will get more time.

Services

At PwC, we are well positioned to support our clients in using CSRD to create value and unlock better performance for their business.

Our CSRD professionals within CEE have global reach. Our team brings together 460+ ESG practitioners across 27 countries in the region, in particular local UA team, and other specialists from across our lines of service give clients depth across the wide range of CSRD requirements.

Moreover, we have a range of digital solutions and alliances. Collecting, analysing and presenting information to make evidence-based decisions with our ecosystem of partners, such as Salesforce, Microsoft, Oracle and SAP.

Our approach is distinguished by flexibility and an individual approach to every client. We harness our experience to provide clients with ongoing recommendations for sustainable development regarding procedures and methodologies.

Contact us