Taxation

Among all the measures announced in the Budget 2019-20, we analysed the impact on the tax areas ranging from corporate to personal tax and immigration.

Browse through the latest tax updates

Corporate Tax Personal Tax Income Exemption Threshold Value Added Tax Other Tax ImmigrationCorporate Tax

- Levy on Companies

- Solidarity Levy on Telephony Service Providers

- Alternative Minimum Tax (AMT) on life insurance business

- Accelerated Depreciation

- Investment Tax Credit (“ITC”)

- Export incentives

- Additional Tax Deduction

- Tax Holidays

- Partial Exemption Regime

- Deferred Duty and Tax Scheme

Levy on Companies

Companies or group of companies having gross income exceeding Rs500m will be subject to levy on their annual gross income as follows:

No levy applicable to companies holding a Global Business Licence and companies in the tourism sector.

Solidarity Levy on Telephony Service Providers

- Solidarity Levy on telephony service providers will be made permanent

Profitable companies will continue to be liable to levy at 5% of accounting profit + 1.5% of turnover

Non-profitable companies will now be liable to levy of 1.5% of turnover

Alternative Minimum Tax (AMT) on life insurance business

Companies carrying out life insurance business will be liable to tax under the existing system or under AMT, whichever is the higher

AMT will be calculated at 10% on the profit attributable to shareholders adjusted for capital gains or losses

Accelerated Depreciation

Accelerated depreciation available on assets acquired as follows:

Investment Tax Credit (“ITC”)

15% ITC available to all manufacturing companies over 3 years

Export incentives

- 50% refund on the costs of certification, testing and accreditation of local laboratories

Additional Tax Deduction

- Double deductions on:

- Plant and machinery acquired by companies affected by COVID-19 during the period 01 March 2020 to 30 June 2020

- Cost of acquisition of patents and franchises including associated costs to comply with international quality standards and norms

- R&D expenditures incurred by Medical R&D centres

Tax Holidays

Double deductions on:

- 8 year tax holiday for companies engaged in:

- Inland aquaculture scheme

- Manufacture of nutraceutical products subject to operations started on or after 04 June 2020

- Manufacture of pharmaceutical products, medical devices or high-tech products if the company has started operations on or after 08 June 2017

- Worldwide institution setting up branch campuses in Mauritius will also benefit from the 8 year tax holiday

Partial Exemption Regime

- 80% partial exemption regime on interest income does not cover the following:

- Non-bank deposit taking institutions;

- Money changers;

- Foreign exchange dealers;

- Insurance companies;

- Leasing companies; and

- Companies providing factoring, hire purchase facilities or credit sale facilities

Deferred Duty and Tax Scheme

- Companies under the Deferred Duty and Tax Scheme and the Mauritius Duty Free Paradise will be allowed to sell their goods on the local market provided they pay taxes

Personal Tax

- Contribution Sociale Generalisee (CSG)

- Solidarity Levy

- Deduction for dependent

Contribution Sociale Generalisee (CSG)

- Introduction of CSG with first payment of benefits in July 2023 to ensure an additional guaranteed monthly income to citizens above 65 years

- Effective as from 01 September 2020, contributions payable under the CSG system are as follows on:

- Monthly salary up to Rs50,000 - 1.5% by employee and 3% by employer

- Monthly salary exceeding Rs50,000 - 3% by employee and 6% by employer

- Introduction of CSG will lead to the abolishment of the National Pension Fund (NPF), however, the NPF will continue to pay benefits to those who have previously contributed to the fund

Reimagine remuneration

It’s time to consider what needs to change within your current remuneration structure to continue attracting and retaining talents.

Solidarity Levy

- Effective from income year 2020-2021, increase in solidarity levy from 5% to 25% on chargeable income plus dividends in excess of Rs3m, excluding lump sum income (pension, death gratuity and death or injury compensation)

PAYE system will apply to collect the solidarity levy

Deduction for dependent

- In addition to the annual income exemption threshold, a taxpayer may now claim a deduction for a bedridden next of kin in his care

Deduction between Rs80,000 to Rs110,000 available provided the number of dependents does not exceed 4

Income Exemption Threshold

Effective as from income year starting on 01 July 2020:

Category |

From (Rs) |

To (Rs) |

Increase (Rs) |

|---|---|---|---|

A. Individual with no dependent |

310,000 |

325,000 |

15,000 |

B. Individual with one dependent |

420,000 |

435,000 |

15,000 |

C. Individual with two dependents |

500,000 |

515,000 |

15,000 |

D. Individual with three dependents |

550,000 |

600,000 |

50,000 |

E. Individual with four or more dependents |

600,000 |

680,000 |

80,000 |

F. Retired/disabled person with no dependent |

360,000 |

375,000 |

15,000 |

G. Retired/disabled person with dependents |

470,000 |

485,000 |

15,000 |

Value Added Tax (VAT)

- Digital and Electronic services

- Pharmaceutical industry

- Blue Economy

- Education

- Construction Sector

- From exempt to zero-rate

Digital and Electronic services

Non-residents providing digital and electronic services through internet for consumption in Mauritius will be subject to VAT

Pharmaceutical industry

VAT exemption for medical research & development centres on construction materials and specialised equipment

Blue Economy

- Inland aquaculture scheme exempt from VAT and duty on equipment

Education

International educational institutions will benefit from VAT exemption on IT and IT related materials and equipment used for online education

Construction Sector

- Payment of VAT from date of receipt instead of date of invoice allowed for Government contracts in relation to construction works

From exempt to zero-rate

- The following exempt items will become zero rated supplies:

- Unprocessed agricultural and horticultural produce

- Live animals of a kind generally used as, or yielding or producing, food for human consumption other than live poultry

- Transport of passengers by public service vehicles excluding contract buses for the transport of tourists and contract car; and

- Medical, hospital and dental services

Other Taxes

- Excise Duty

- Customs Duty

- Increase in duties and taxes on gambling

- Property Tax

Excise Duty

As from 05 June 2020, excise tax on sugar sweetened products will be doubled to 6 cents per gram and extended to specified locally manufactured and imported non-staple sweetened products

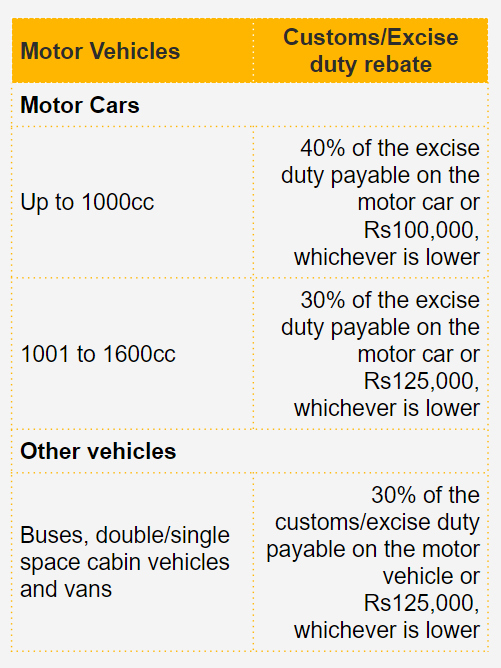

- A rebate on the amount of customs/excise will be granted on vehicles, provided they were in bonded warehouse before 05 June 2020 and are cleared from Customs before 30 June 2021.

Customs Duty

Exemption value of article imported by post or courier services reduced from Rs3,000 to Rs1,000.

Rate of customs duty on import of sugar will be increased from 80 percent to 100 percent.

Increase in duties and taxes on gambling

Property Tax

The scheme regarding exemption from registration duty on acquisition of a newly-built dwelling will be extended to 30 June 2022 and value of the property will be raised to Rs7m. The exemption will also cover purchases on the basis of a plan or during construction but has certain exclusions

Exemption from land transfer tax to a promoter undertaking construction of housing projects of at least 5 residential units for Mauritians will be extended to 31 December 2020. No registration and land transfer tax will be payable on the transfer of freehold bare land for the construction of housing projects provided the land is transferred by 31 December 2020 and construction completed by 31 December 2021. Exemption of land transfer tax will be granted on sale of residential unit made to a Mauritian before 30 June 2022.

- A person is now eligible to first-time buyer registration duty exemption if he or his spouse is or was the:

- owner of an immovable property acquired by inheritance where the land is less than 20 perches

- co-owner of an immovable property acquired by inheritance where their share in that property is less than 20 perches of land

Tax Administration

- General

- Income Tax

- Value Added Tax

- Customs

- Suspected cases of infringement of industrial rights

- Customs Tariff

General

- Tax Account Number (TAN)

Each citizen will automatically receive a TAN

- Assessment Review Committee (ARC)

Where an aggrieved taxpayer repeatedly fails to attend or to be represented upon convened, the ARC will strike out the case if such failure is not due to illness or other reasonable cause

- Acquisition of residential unit from National Empowerment Foundation (NEF)

Exemption from payment of registration duty on acquisition of a residential unit from the NEF by an individual who is registered on the Social Register of Mauritius

Income Tax

- Income tax refund by the MRA

Time limit to effect income tax refunds standardised to 60 days for all taxpayers as from the date all necessary documentation pertaining to the application is received by the MRA

- E-services platform

MRA to further develop its e-services platform to improve efficiency and transparency in service delivery to taxpayers

Value Added Tax

Market value of the supply will be taken as the taxable value where a transaction is not at arm’s length

VAT-registered person making both taxable and exempt supplies may apply for an alternative basis to apportion input tax where he is engaged in a project spanning over several years

Administrator, executor, receiver or liquidator to inform the MRA within 15 days of his appointment for the management or winding up of the business of a taxable person

Provisions will be made to allow a claim for VAT refund below Rs25,000 in respect of a residential building subject to the amount of VAT paid during a quarter and preceding three quarters does not exceed Rs25,000

Introduction of a VAT e-invoicing at business level on a pilot basis

Customs

Principal Officer of a private company (may be the executive director or any other person who is entitled to exercise the powers of the Boards of directors) will be liable for any taxes due by the company

The time frame of 28 days to settle underpayment of duties, excise duties, taxes and penalties by an importer/manufacturer extended to cover the following:

default on deferred payment facilities

non-submission of cargo report for an aircraft or ship

importation of selected prohibited goods

Goods imported in multiple consignments or shipments to be assembled into a complete finished good such as a photovoltaic system or a greenhouse will be classified under the same category as the finished products for tariff purposes

Customs declarations (Bill of Entry) made in respect of imports will be deemed to be a self-assessment

A penalty Rs500 per day of non-compliance up to a maximum of Rs5000 will be imposed on master, owner or duly authorised agent of an aircraft or ship failing to give a cargo report in respect of the aircraft or ship, its craft and passengers.

Qualified person from a Freight Forwarding Agent company will be authorised to act as broker by the MRA

Suspected cases of infringement of industrial rights

Public notice will be given where the MRA customs suspends the clearance of imported goods or detains goods on the local market

No future suspension of the clearance of imported goods or detention of goods on local market will be made by the MRA unless and until the right holder initiates legal proceedings

Customs Tariff

Rate of exchange to be used for valuation purposes will now be posted on the MRA’s website

Immigration

- Investments

- Duration of Permits

- Dependents

- Non-Citizen Professionals

- Administration

Investments

- Initial investment of USD100,000 required to be eligible for an Occupation Permit as investor has been reduced to USD50,000

Minimum investment of USD40,000 required to be eligible for an Innovator Occupation Permit is being removed as well as the minimum turnover requirement

Holders of Occupation Permits (OP) and Residence Permits as Retired Non Citizens will not have any shareholding restrictions to invest in other ventures

Duration of Permits

Occupation Permits and Residence Permits as Retired Non Citizens can be applied for a maximum period of 10 years renewable

Permanent Residence Permit will be valid for 20 years

Dependents

- No permit is required for the spouse of an OP holder to be able to invest or work in Mauritius

Parents of OP holders will be allowed to live in Mauritius

Non-Citizen Professionals

- Minimum monthly salary of Rs30,000 for ICT professionals to obtain an Occupation Permit will be extended to other sectors

Work Permit and Residence Permit will now be issued as one permit instead of two separate documents

Administration

- Occupation Permit applications will be determined and recommended by the Economic Development Board only

Our #Budget20 is one click away...

Subscribe to receive our Budget 2020 Brief with our overall opinion on the measures, a tax perspective, and reviews of the top sectors in Mauritius.

Subscribe to receive

Contact us

Anthony Leung Shing, ACA, CTA

EMA Deputy Regional Senior Partner, Country Senior Partner, PwC Mauritius

Tel: +230 404 5071

Follow PwC Mauritius