Post-COVID-19 transformation

Back in 2013, PwC identified five long-term powerful and interdependent megatrends that are expected to fundamentally reshape the world and the GCC region over the next decade:

Demographic and social change

Resource scarcity and climate change

Shift in power east

Rise of technology

Urbanisation

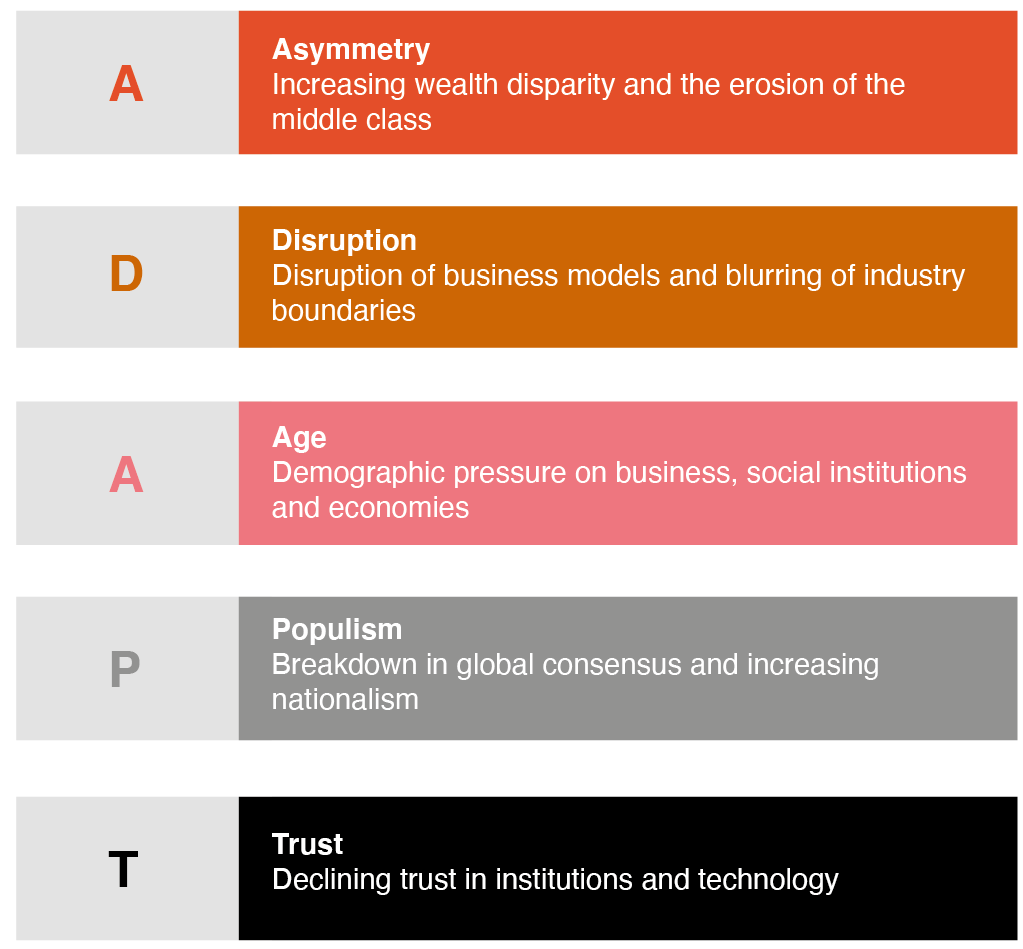

Even prior to COVID-19, leaders needed to respond quickly, changing their strategies to address these megatrends. We captured these in our ADAPT framework. Both globally and locally, the pandemic has intensified the ADAPT forces, catalysing change at an even greater speed.

Impact on Qatar

In Qatar, the pandemic accelerated the impact of these five forces, increasing pressure for localising the workforce, testing institutional ability to respond, and renewing the importance of digitisation, sustainability and self-sufficiency. Overall, the additional pressure added to the sense of urgency for economic diversification plans for all GCC countries, pushing policymakers to redouble efforts on issues such as the development of a strong private sector, upskilling the local talent, localisation of supply chains and faster digital transformation.

Despite the magnitude of the crisis, Qatar has several advantages to mitigate these challenges. Qatar Investment Authority’s assets provide a backstop, if needed, to absorb economic shocks and support economic transformation plans. The restoration of this year’s travel and trade ties with neighboring GCC countries supported Qatar’s regional integration in contrast to the growing global polarisation trends.

Another significant strength has been the trust in institutions, which has remained strong throughout the pandemic as the government proactively managed the crisis with minimal disruption in the healthcare system.

Six economic transformation themes in Qatar

To rebuild the economy, the Qatari government will have to step in with several policies, including those related to six transformation themes: Diversification and private sector development; Fiscal management and innovation; Digitisation; Glocalisation and talent attraction; Value creation; Energy transition and sustainability. Each of these themes has relevance for the post-pandemic economy.

- Diversification and Private Sector Development

- Fiscal Management and Innovation

- Digitisation

- Glocalisation and Talent Attraction

- Value Creation

- Energy Transition and Sustainability

Diversification and Private Sector Development

Qatar National Vision 2030, published in 2008, and the 2019 Economic Diversification and Private Sector Development (EDPSD) strategy have provided the framework for the government’s efforts to diversify the economy, emphasising productivity, competitiveness and private sector-led growth.

Thirteen years later, the State of Qatar has made concrete strides towards diversification, including through reforming the business environment and increased government spending on large-scale infrastructure development ahead of World Cup 2022. The creation of institutional bodies such as Qatar Financial Center, Qatar Free Zones Authority and Qatar Science and Technology Park (QSTP) together with the amendment of its laws surrounding foreign ownership have created new routes for investment. These efforts have been reflected in the 2019 World Economic Forum Global Competitive Report wherein Qatar ranks second in the region and 29th globally for its overall competitiveness.

The Public Private Partnership Law, issued in May 2020, is expected to enhance opportunities in various sectors including education, healthcare, real estate, tourism, power and utilities. Public sector procurement initiatives will also contribute to private sector development, including Qatar Petroleum’s flagship Tawteen localisation program. This comes as the private sector has been boosting its self-reliance recently, with success stories such as Baladna and QDB’s work to develop small and medium enterprises.

Looking forward, as the economies in the region come out of the aftermath of the pandemic, there is little doubt that they will need to move swiftly to tackle the challenges that lie ahead. Qatar has already shown its resilience and the building blocks that have been put in place will undoubtedly help create sustainable growth in the future.

Getting from 2022 to 2030

At the time of writing, Qatar’s COVID-19 cases have fallen to their lowest level since the start of the pandemic and focus is shifting to the next stages of development. The World Cup next year is an obvious focus and the startup of the new LNG trains from 2025 will be a major driver of the economy. But the longer-term trajectory, working towards the goals of a more diversified and sustainable society, as outlined in Vision 2030, will depend on making progress on the six themes above to drive economic transformation and respond not only to immediate challenges, like pandemics and volatile energy prices, but the broader challenges presented by the megatrends.

Related content

Contact us

Follow us